Manner in which chargeable income is to be ascertained P ART III ASCERTAINMENT OF CHARGEABLE. Interpretation P ART II IMPOSITION OF THE TAX 3.

Different Types Of Income Tax Assessments Under The Income Tax Act

1 Subject to this Ordinance income tax shall be imposed foreach tax year at the rate or rates specified in Division I or II of Part I ofthe First Schedule as the case may be on every person who has taxable incomefor the year.

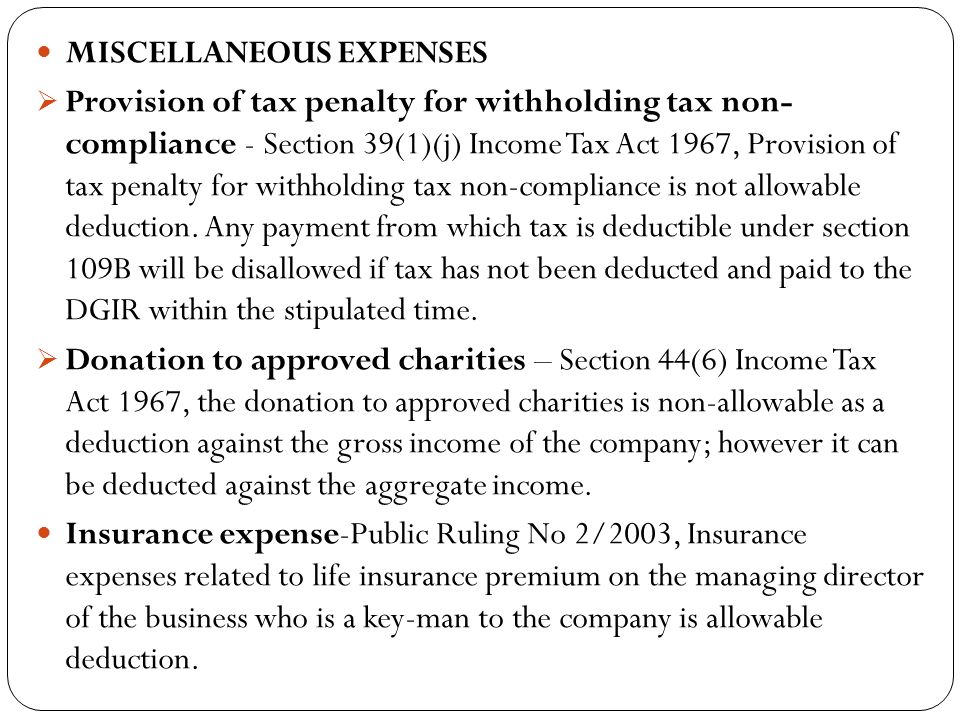

. Any particular dealing or transactions must come within the walls of scope. The Income Tax Act 1967 which is referred to as the principal Act in this Chapter is amended in subsection 51a by. Amendment of section 131 25.

In Malaysia income tax is generally governed by Income Tax Act 1967 Act 531967. For the purpose of paragraph 4a gains or profits from a business shall include an amount receivable arising from stock in trade parted with by any element of compulsion including on requisition or compulsory acquisition or in a similar manner. Amendment of section 127 24.

Short title and commencement. Or Income Tax Act 1967. Federal Legislation Portal Malaysia.

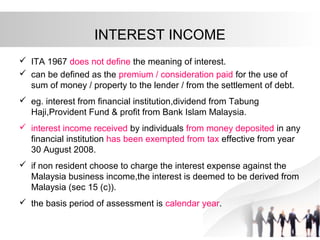

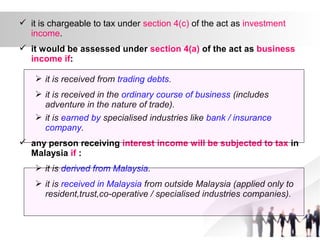

Tax on taxable income-. Income falling under paragraph 4 f chargeable to tax 41 The introduction of a new section 109F of the ITA with effect from 01012009 provides a mechanism to collect withholding tax from a non-resident person who receives income which is derived from Malaysia in respect of gains or profits that fall under paragraph 4 f of the ITA. Charging section Section 4 of the Income-Tax Act 1961 is the Charging section of the Act.

Individuals who own a property in Malaysia that isnt used for business purposes and receive a rental income are subject to income tax. 12 Where an operator carrying on general business has re-takaful the risks or part of the risks with a re-takaful operator who either does not carry on the business of takaful of that kind in Malaysia or does not re-takaful the risks through a branch in. New section 109da 22.

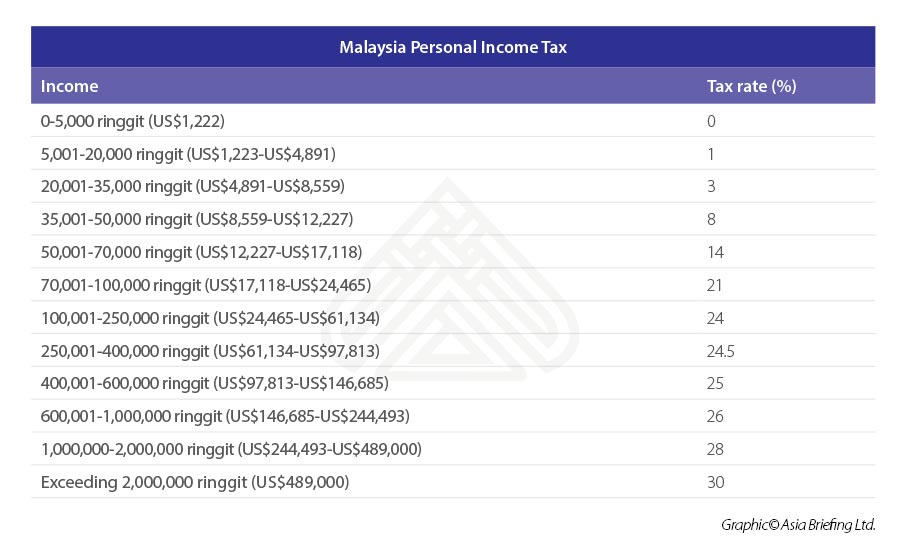

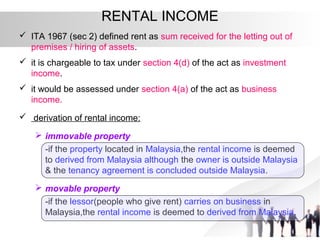

An income tax rebate is calculated at the end section of your BE form after youve determined the amount of tax charged on your chargeable income. 2 The income tax payable by a taxpayer for a tax year shallbe computed by applying the rate or rates of tax applicable to the. Where the property concerned is managed and let in such a systematic or organized manner that the letting can be regarded as carrying on a business the income from the letting can be charged to tax under section 4a of the Act.

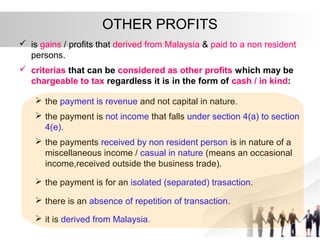

It will also give the readers an overview of what is income in revenue law. Gains or profits from a business arising from stock in trade parted with by any element of compulsion. Income falling under Section 4f of the Income.

A b c d e f Business. D rents royalties or premium. 1 Subject to this section income tax charged for each year of assessment upon the chargeable income of a person who gives any loan to a small business shall be rebated by an amount equivalent to two per cent prorated per annum or such other rate as may be prescribed from time to time by the Minister on the outstanding balance of the loan before any set off is made under.

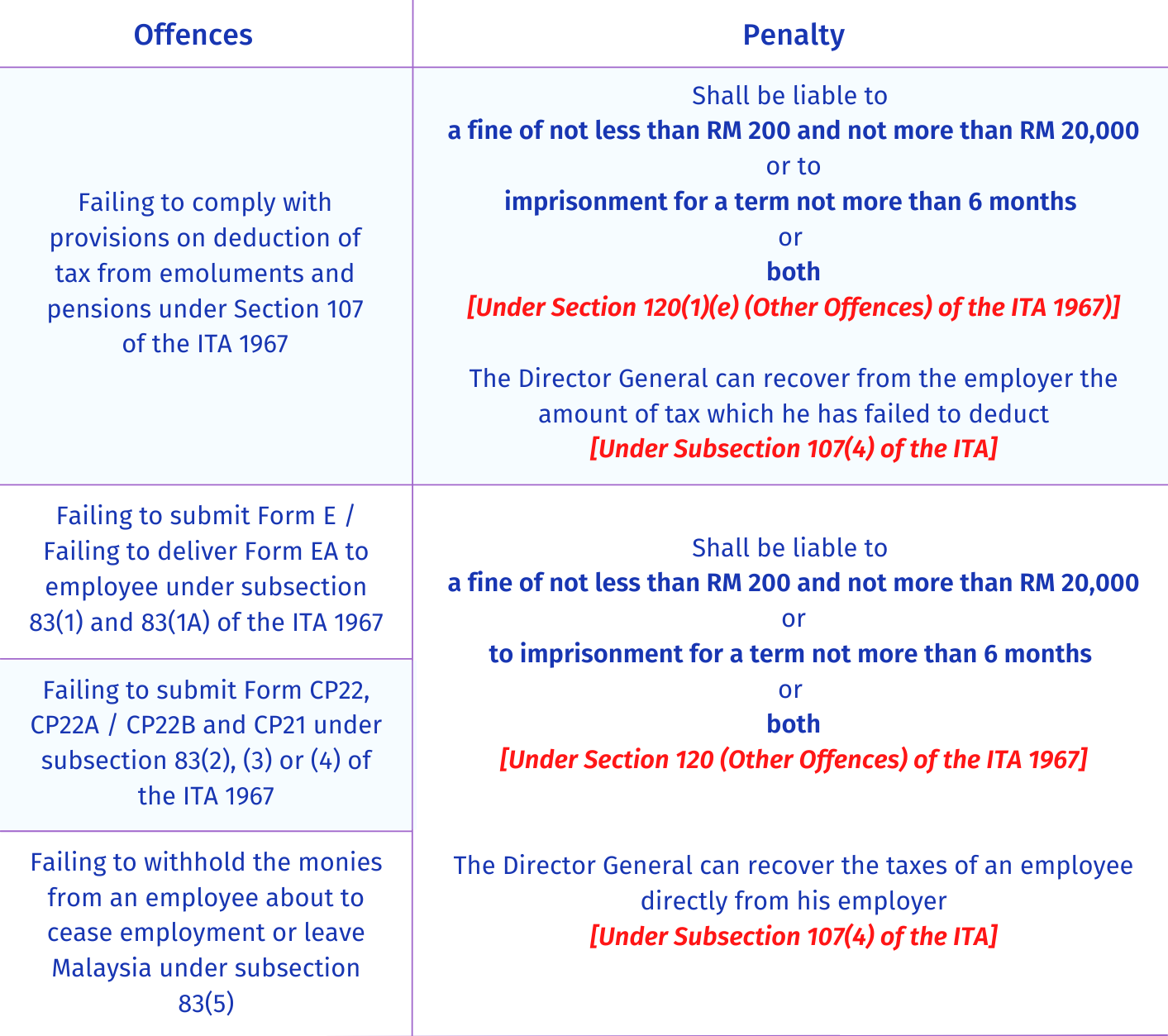

The new guidelines are broadly similar to the earlier guidelines and explain the penalties that will be imposed under Section 1123 of the Income Tax Act 1967 ITA Section 513 of the Petroleum Income Tax Act 1967 PITA and Section 293 of the Real Property Gains Tax Act 1976 RPGTA where a taxpayer fails to furnish a tax return within. 1 This Act may be cited as the Income Tax Act 1967. When rental income is assessed under section 4 d it has to be grouped into three sources namely residential.

E following classes of income are liable to income tax pursuant to Section 4 of the Income Tax Act 1967. So the first thing you need to take note of is how the income from your property rental is calculated. And often allow notional reductions of income.

11 The adjusted income as ascertained under subsections 9 and 10 shall be deemed to be the statutory income from that source. This page is currently under maintenance. Get Returns as high as 15 Zero Capital Gains tax.

Dividends interest or discounts. This is explained in greater detail under Section 4 d of the same Act. Short title extent and commencement 2.

And references in this section to income in relation to any settlement or arising under the settlement. Income tax under section 4d of the Act. Reference to the updated Income Tax Act 1967 which incorporates the latest amendments last updated 1 March 2021 made by Finance Act 2017 Act 785 can be accessed through the Attorney Generals Chamber Official Portal at the following link.

4 Laws of Malaysia ACT 833 21. LAWS OF MALAYSIA Act 543 PETROLEUM INCOME TAX ACT 1967 ARRANGEMENT OF SECTIONS P ART I PRELIMINARY Section 1. Clue of what section 4 Income Tax Act 1967 trying to classify.

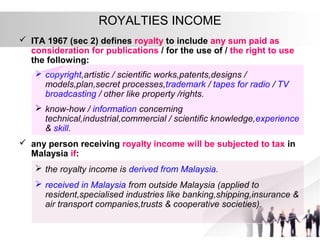

Rents royalities or premiums. 3 This Act shall have effect for the year of assessment 1968 and subsequent years of assessment. Income under Section 4f ITA 1967.

Classes of income on which tax is chargeable. Rental income is generally assessed under Section 4 d Rental Income of the Income Tax Act and is seen as income from investment. Rental income is generally assessed under Section 4d Rental Income of the Income Tax Act and is seen as income from investment.

Subject to this Act the income upon which tax is chargeable under this Act is income in respect of-a gains or profits from a business for whatever period of time carried on. Rent as a business source. Income Tax Act 1959.

Unannotated Statutes of Malaysia - Principal ActsINCOME TAX ACT 1967 Act 53INCOME TAX ACT 1967 ACT 5382ADuty to keep documents for ascertaining chargeable income and tax payable. Charge of petroleum income tax 4. B gains or profits from an employment.

Pensions annuities or other periodical payments not falling under any of the foregoing paragraphs. Amendment of section 131a. Amendment of section 120 23.

Unannotated Statutes of Malaysia - Principal ActsINCOME TAX ACT 1967 Act 53INCOME TAX ACT 1967 ACT 532Interpretation. When rental income is assessed under section 4 d it has to be grouped into three sources namely residential properties commercial properties and vacant land. Unannotated Statutes of Malaysia - Principal ActsINCOME TAX ACT 1967 Act 53INCOME TAX ACT 1967 ACT 5363CSpecial treatment on rent from the letting of real property of a Real Estate Investment Trust or Property Trust Fund.

Every person who in whatever capacity is in receipt or has control of any money or property being income of the kind mentioned in section 4 of or belonging. Amendment of section 5 4.

Taxation Principles Dividend Interest Rental Royalty And Other So

Taxation Principles Dividend Interest Rental Royalty And Other So

Problem Based Learning Project Tax Computation On Malaysian Food Service Mfs Sdn Bhd Group B Namematrik No Izwani Bt Abdul Majid Hazwani Bt Ghazali Ppt Download

Problem Based Learning Project Tax Computation On Malaysian Food Service Mfs Sdn Bhd Group B Namematrik No Izwani Bt Abdul Majid Hazwani Bt Ghazali Ppt Download

Guide To Tax Clearance In Malaysia For Expatriates And Locals Toughnickel

Individual Income Tax In Malaysia For Expatriates

2

Tax And Investments In Malaysia Crowe Malaysia Plt

Taxation Principles Dividend Interest Rental Royalty And Other So

Taxation Principles Dividend Interest Rental Royalty And Other So

Taxation Principles Dividend Interest Rental Royalty And Other So

Problem Based Learning Project Tax Computation On Malaysian Food Service Mfs Sdn Bhd Group B Namematrik No Izwani Bt Abdul Majid Hazwani Bt Ghazali Ppt Download

Wholesale Retail Trade Wrt License In Malaysia Malaysia Small Business Ideas Export Business

Overview Of Malaysian Taxation By Associate Professor Dr Gholamreza Zandi Ppt Download

Pdf Complexity Of The Malaysian Income Tax Act 1967 Readability Assessment

As An Employer What Are Their Obligations In Terms Of Income Tax

Taxation Principles Dividend Interest Rental Royalty And Other So

Taxation Principles Dividend Interest Rental Royalty And Other So

Business Income Tax Malaysia Deadlines For 2021

- tulang rusuk yang lama hilang

- sayang papa saya tak?

- motor roda tiga bekas solo

- lirik cinta ismail izzani

- gambar kedai jus

- sunblock terbaik untuk badan dan wajah

- contoh lukisan tahun 2

- uncle muthu upin ipin

- ruang bilik tidur idaman

- objektif rancangan pengajaran harian

- janam janam lirik arti

- dapur gas mr diy

- lee perara & tan

- surat lamaran kerja email

- tv box q plus

- pie ayam keju

- alat pelindung diri petugas kebersihan

- karbohidrat ringkas

- wira convert evo 3 untuk dijual

- soalan tatabahasa tahun 4